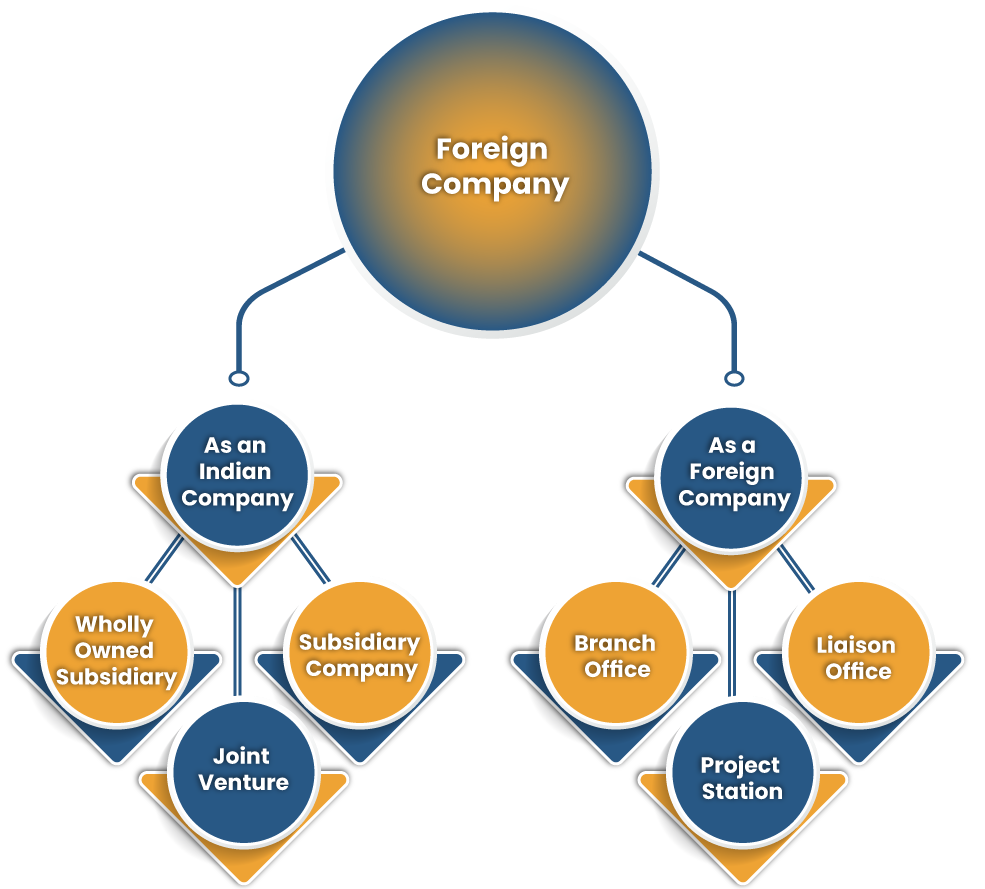

When Indian Companies are treated as Foreign Companies

Provisions Related to Foreign Company" />

Provisions Related to Foreign Company" />

In this article, the author shares with you all the applicable provisions on Foreign Company.

There are various types of companies like public companies, private companies, One person company, Government companies, subsidiary companies and one of them is FOREIGN COMPANY , operating in our country. The distinction is based on their specific nature or capital or ownership and on various applicable rules and regulations and provisions on each types of companies.

Every country has their particular rules and regulations which are applicable on their home country's companies. Any company, doing their business in country other than home country is bound to comply with the rules and regulations of that particular country or areas and the home country where it was originally incorporated.

In our Country, All the companies which are not domestic or which are foreign companies are bound to comply with the certain rules , regulations, laws as compared to a domestic companies. Some of the acts are like FEMA law , Income Tax law , Company Law , RBI law and regulations etc.

FOREIGN COMPANY

A 'foreign company' is an entity which is incorporated outside India, but has a place of business in India or conducts any business activity in India in any other manner. The Complete definition of foreign company is given under the Companies Act, 2013 though the concept of 'foreign company' was existent in the older act as well. Under the companies Act 2013 the concept of foreign company is given in broad manner , scope of foreign companies increased.

Features of Foreign Company

The major features of foreign collaboration for the growth of business are as follows:

- Agreement: Foreign collaboration is an agreement or contract between two or more companies from different countries for mutual benefit.

- Government consent: Foreign collaboration is now recognized as an important driver of growth in the country. Foreign collaboration requires Government approval, as the collaboration involves partnership between two countries. Some legal formalities are to be fulfilled to enter into a contract. That requires government permission.

- World integration: Globalisation means integration of world economy, where the world becomes a single market. Foreign collaboration allows different countries to enter into partnership and reap the benefit. It helps both the developed and developing countries to come together to achieve the common objectives and maintains international peace.

- Growth of industrial sector: Foreign collaboration leads to growth of industries of the countries coming into contract. Foreign collaboration develops industries and increases employment opportunities, thereby improving the working conditions of the masses.

- Gives legal Identity: Foreign collaboration is a legal entity between two or more parties for a particular purpose or venture.

- Helps to meet out requirements: Interdependence among countries is a common phenomenon these days. Foreign collaboration is very useful in meeting out the deficiencies of the resources and in getting advanced technology with competitive price.

Definition of Foreign Company under Companies Act, 2013 and its scope

The term 'foreign company' is clearly laid down under Section 2 sub-section 42 of the Companies Act, 2013 (New Act). A foreign company is any company or body corporate incorporated outside India which,

- Has a place of business in India whether by itself or through an agent, physically or through electronic mode; and

- Conducts any business activity in India in any other manner.

In order to be considered a 'foreign company', one has to fulfil both the abovementioned criteria. Hence, this new definition has a wider scope compared to the earlier Act. To fully appreciate the scope of the definition, it is necessary to define the terms 'electronic mode' as well as 'business activity'.

Electronic Mode

- The Companies (Specification of Definitions Details) Rules, 2014 defines the term 'electronic mode' in the context of a foreign company under Rule 2(h).

- The definition of electronic mode encompasses all electronic based transactions, such as business to business and business to consumer transactions, data exchange and other digital supply transactions. It further includes all online services and all related data communication services whether conducted by e-mail, mobile devices, cloud computing, social media, data transmission or otherwise.

This definition clearly states that even if the location of the main server is outside India, it would still come within the purview of the term 'electronic mode'. Hence, leaving no ambiguity in its interpretation.

Business Activity

- The Companies (Registration Offices and Fees) Rules, 2014, defines 'business activity' under Rule 3. The definition of 'business activity' is identical to 'electronic mode'. Rule 3 states that every company including a foreign company that carries out its business through electronic mode, whether its main server is installed in India or outside India, shall be deemed to have carried out business in India.

- However, the definition of 'electronic mode' is applicable to only foreign companies whereas, the definition of 'business activity' is applicable to all kinds of companies.

By virtue of this definition of 'foreign company' under the Companies Act, 2013, even a foreign e-commerce website based outside India, not having any office, employees, servers, or any other sort of physical presence in India would attract the provisions of the Companies Act, 2013, if an Indian resident placed an order on such merchant website.

Impact of the New Definition of Foreign Company under Companies Act

The impact of the definition of foreign companies under the New Act has been two fold.

- First, as the scope of the definition has expanded, it covers various companies that were before eluded from the scope of the Companies Act.

- Second, the statutory compliance of the foreign companies have increased under the new act.

Wider Scope

The ambit of term 'electronic mode' under the definition of foreign company is extensive enough to cover essentially all transaction carried through electronic mode.

Further, the second part of the definition of foreign company refers to any other 'business activity' which will now include companies in media and broadcasting business. This will have huge implications on such business as they will have the burden of adhering to statutory compliance under the companies act, 2013.

Increased Compliance

The foreign companies incorporated outside India always had some provisions of the Companies Act, 1956 being applicable to them under the Part XI. Such foreign companies which would have established a place of business in India before or after the commencement of the Old Act had to comply with some of the provisions of Old Act which included submitting with the registrar charter documents of the place of business in India, its address, details of directors etc. for registration, accounts of the Indian entity, details of charges made on property in India and so on.

Particulars Relating to Directors and Secretary to be Furnished to the Registrar by Foreign Companies

- Every foreign company shall, within thirty days of establishment of its place of business in India, in addition to the particulars specified in sub-section (1) of section 380 of the Act, also deliver to the Registrar for registration, a list of directors and Secretary of such company.

- The list of directors and secretary or equivalent (by whatever name called) of the foreign company shall contain the following particulars, for each of the persons included in such list, namely:-

(a) personal name and surname in full;

(b) any former name or names and surname or surnames in ffull

(c) father's name or mother's name and spouse's name;

(d) date of birth;

(e) residential address;

(f) nationality;

(g) if the present nationality is not the nationality of origin, his nationality of origin;

(h) passport Number, date of issue and country of issue; (if a person holds more than one passport then details of all passports to be given)

(i) income-tax permanent account number (PAN) , if applicable;

(j) occupation, if any ;

(k) whether directorship in any other Indian company, (Director Identification Number (DIN), Name and Corporate Identity Number (CIN) of the company in case of holding directorship);

(l) other directorship or directorships held by him;

(m) Membership Number (for Secretary only); and

(n) e-mail ID.

- A foreign company shall, within a period of 30 days of the establishment of its place of business in India, file with the registrar Form FC-1 with such fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and with the documents required to be delivered for registration by a foreign company in accordance with the provisions of sub-section (1) of section 380 and the application shall also be supported with an attested copy of approval from the Reserve Bank of India under Foreign Exchange Management Act or Regulations, and also from other regulators, if any, approval is required by such foreign company to establish a place of business in India or a declaration from the authorised representative of such foreign company that no such approval is required.

- Where any alteration is made or occurs in the document delivered to the Registrar for registration under sub-section (1) of section 380, the foreign company shall file with the Registrar, a return in Form FC-2 along with the fee as provided in the Companies (Registration Offices and Fees) Rules, 2014 containing the particulars of the alteration, within a period of 30 days from the date on which the alteration was made or occurred.

The provisions applicable to the foreign companies have now been widened, any charge created by such foreign company will have to be registered with the Registrar of Companies. They are further bound to file a statement with regard to related party transactions, repatriation of profits, etc. and get its accounts audited by a practicing Chartered Accountant in India. The new requirements of registration and other compliance will again have an impact on the operation of various companies, as it will acts as an increased burden on the foreign companies.

Amendment of 2017

- Section 379 of the 2013 Act laid down that where not less than 50% of the paid up capital of a foreign company is held by one or more citizens of India, or companies/body corporates incorporated in India, such company has to comply with the provisions of Chapter 22 and other provisions of the 2013 Act, as may be prescribed, with regard to the business carried on by it in India, as if it was a company incorporated in India.

- It failed to clarify whether Chapter 22 referring to 'companies incorporated outside India' applied to all foreign companies. The bare perusal of the provisions makes it clear that after defining 'foreign companies' in a comprehensive manner, the intention of the legislature was not to restrict the scope of applicability of Chapter 22 to a specific class of companies.

- There was an urgent need to fulfill the same gap before the foreign companies could use the same lacuna in order to avoid their statutory compliance. This issue has been finally addressed by the Companies (Amendment) Act, 2017.

This amendment clarified that Chapter 22 of the 2013 Act would be applicable to 'all the foreign companies' irrespective of any other condition. This amendment further empowered the Central Government to exempt any class of foreign companies from complying with one or more provisions of the 2013 Act.

Conclusion

- The 2013 Act and the recent amendments have clarified the scope of definition of 'foreign companies' to a large extent. The definition of the term 'foreign company' under the Companies Act, 2013 read with the definition of 'electronic mode', could result in insignificant internet based electronic transactions of a company incorporated outside India, with no adequate relation to Indian customers and no establishment in India would deem to fall under the ambit of such definition. It was further assumed that it would be impracticable to cover companies incorporated outside India that have a mere incidental presence in India through electronic means, without the company having any actual intention of setting up a place of business in country. In light of this, it was suggested that the same be exempted from registration and other statutory requirements applicable to foreign companies under the Companies Act, 2013.

- Further to such recommendations of the Committee, Among the crucial amendments proposed under the Companies (Amendment) Bill, 2016, was the proposed amendment to Section 379 of the 2013 Act stating that “…Foreign companies having incidental transactions through electronic mode to be exempted from registering and compliance regime under the Act.”

- However, the amended Section 379 does not refer to exclusion of incidental transactions. Moreover, no Order under the proviso to amended Section 379 of the Companies Act, 2013 has been introduced in the public domain, referring to the same. Hence, the issue relating to incidental transactions still persists.

Accordingly as above stated provisions it is pertinent to mention that, the enactment of Amendment Act of 2017 has to an extent limited the overarching scope of definition of foreign company, but still there is scope of improvement in the given definition of 'foreign company' under the Companies Act, 2013.